Pre-Arbitration and Arbitration Process

Pre-Arbitration

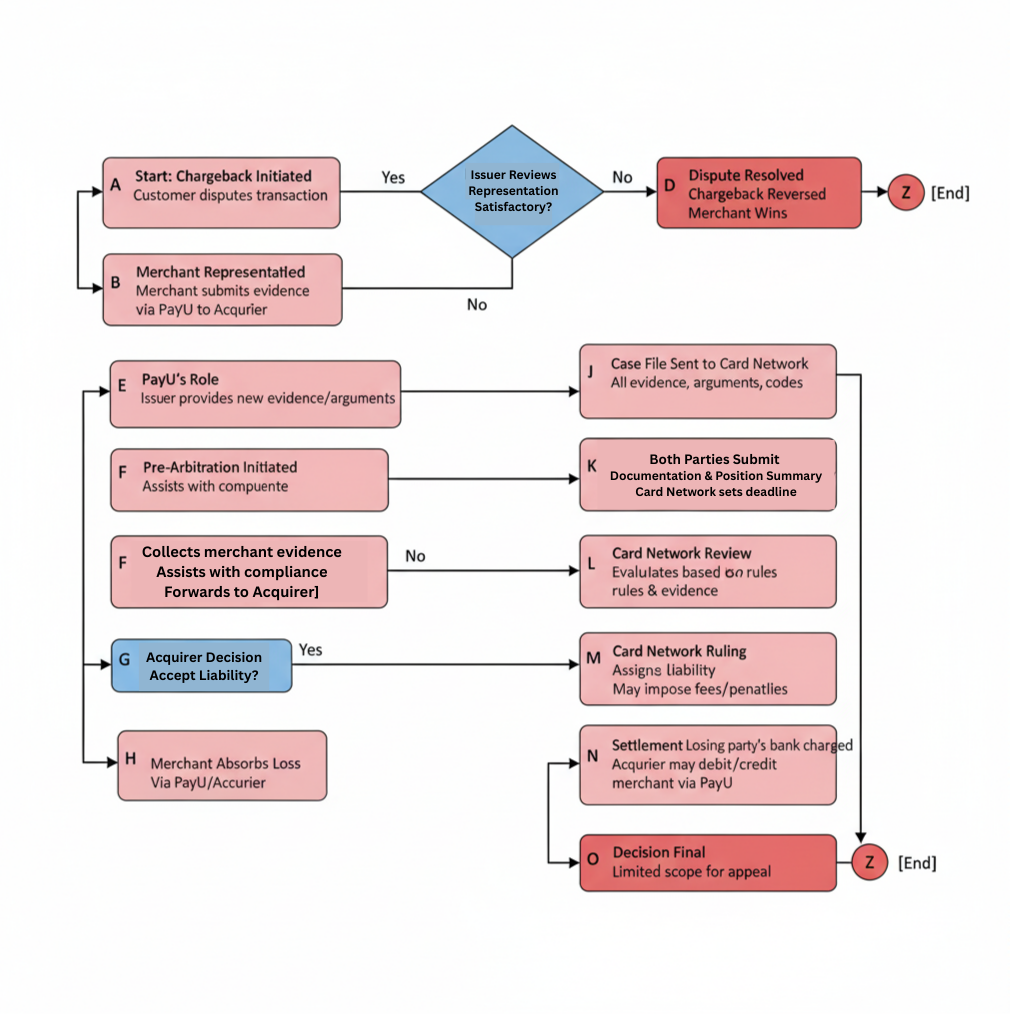

After the merchant/acquirer has represented the case (submitted evidence) and the issuer still disagrees with the response. This offers a final opportunity to resolve the dispute based on new information or further clarification, potentially avoiding formal arbitration. The following happens with the case:

-

The issuer (customer’s bank) initiates pre-arbitration, usually providing new evidence or arguments as to why the chargeback should stand.

-

The acquirer (merchant’s bank through PayU) receives this and can:

- Accept (agree with chargeback, absorbing the loss), or

- Decline (dispute further, escalating to arbitration).

All additional correspondence, documentation, and clarified arguments are exchanged between issuer and acquirer, often facilitated or relayed by the PayU.

Arbitration

If pre-arbitration does not resolve the dispute—that is, the acquirer declines to accept liability. Issuer now formally intervenes and reviews the complete dispute file. The following happens with the case:

- Both parties (issuer and acquirer) submit all documentation, correspondence, and a summary of their positions.

- Issuer dispute resolution team evaluates according to rules and evidence.

- Issuer issues a ruling: assigns financial liability (who bears the loss) and may impose administrative fees or penalties.

- The decision at this stage is final and binding.

Workflow

-

Role of PayU:

- Acts as an intermediary, collecting all merchant evidence and forwarding it to the acquirer (merchant’s settling bank, e.g., ICICI, HDFC, etc.).

- PayU assists in interpreting chargeback codes, compliance criteria, and documentation for the acquiring bank’s submission.

-

If Pre-Arbitration Is Initiated:

- The issuing bank, after reviewing the merchant’s representment (initial defense), may still find the defense unsatisfactory or provide new evidence.

- The issuer sends a pre-arbitration claim to the acquirer.

- PayU coordinates with the merchant (if more evidence is required) and the acquiring bank decides whether to accept liability or pursue further.

- If accepted, the merchant (indirectly, through acquirer/PayU) absorbs the financial loss.

- If declined, the process moves to arbitration.

-

During Arbitration:

- The dispute case file—including all prior evidence, chargeback codes, written arguments, and any newly exchanged materials—is sent to card issuer for adjudication.

- Card issuer sets a deadline for both sides to submit any additional evidence/arguments.

- Card issuer's ruling is communicated back to the acquiring and issuing banks.

- Any imposed fees (arbitration costs, penalties for losing party) are charged to the losing side’s bank, which may then debit/credit the merchant via PayU.

-

Timeline and Finality:

- Timeframes for responses and escalation are strictly governed by Card issuer's rules (often 45-60 days for each stage).

- Once Card issuers has ruled, there is very limited scope for appeal.

- The result is enforced through settlement systems, adjusting balances between acquirer, issuer, and, eventually, merchant.

| PayU’s Role | Acquirer’s Role | Merchant’s Part | |

|---|---|---|---|

| Pre-Arbitration | Forwards case, may request docs | Accept/Decline liability | May provide new/further supporting docs if asked |

| Arbitration | Relays final case, informs outcome | Engages with Mastercard | Accepts final outcome, no further recourse |

| Compliance | Advises on rules/guidelines | Ensures rule adherence | May need to provide docs for compliance cases |

| Fees/Penalties | Passes fees (if any) onward | Pays/recovers from merchant | Pays/recovers if liable |

Updated about 6 hours ago